Microchip Technologies: High Risk, Low Reward

I must confess that our 21% gain on put options in Microchip Technology Incorporated (MCHP) back in April makes it rather enjoyable strolling down memory lane to write about this company again. In my view, it’s time to return to the well as once again the shares look overvalued and there might very well be some money to be made by buying puts on this name. Those less interested in actively profiting from this move should simply avoid the company at the moment. I’ll go through my logic below, with an eye to trying to make a reasonable forecast for future prices. In sum, the problems that I referenced earlier not only linger, but have gotten somewhat worse in my opinion.

Financial Snapshot

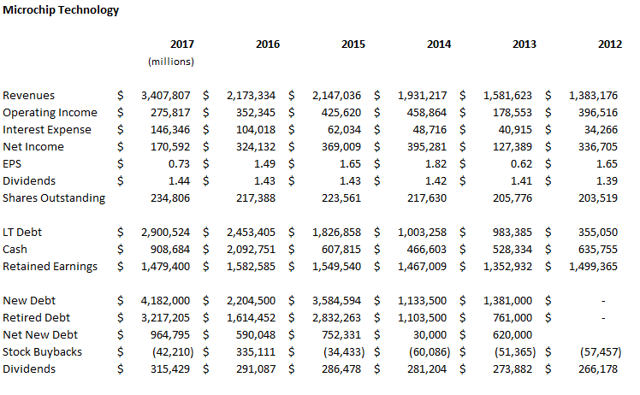

A few things leap off the page when I conduct a quick review of the financial statements at Microchip. One thing that is immediately apparent is the continued tenuous relationship between revenue and net income. For the most recent period, revenue is up about 56%, while net income is down about 48%. I made note of the disconnect in my earlier article, asking the question “if rising revenues won’t lead to improved profitability, what on Earth will?” On the other hand, free cash flow per share continues to rise, as the company continues to acquire other businesses. What fans of free cash flow may be less aware of is the idea that this marginal improvement in free cash flow comes with the added risks associated with acquisitions, so from the shareholder's point of view, the exercise might be called a wash. In my view, investors shouldn’t concern themselves with simple “growth.” They need to concern themselves with risk adjusted growth. In terms of Microchip, I don’t see it.

Turning to the capital structure, the debt level is up sharply again. It has grown at a CAGR of about 42% since 2012, and it seems that management has no interest in paying it down. At the same time, interest expense has grown from about $34 million a year in 2012, to about $146 million a year today. One thing that is far more certain than the “synergies” delivered from various acquisitions is the fact that interest expense is now about 85% of net income. At some point, the debt here will slow dividends or the company’s ability to continue to grow by acquisition. That’ll be a painful day for shareholders in my view.

Turning to the capital structure, the debt level is up sharply again. It has grown at a CAGR of about 42% since 2012, and it seems that management has no interest in paying it down. At the same time, interest expense has grown from about $34 million a year in 2012, to about $146 million a year today. One thing that is far more certain than the “synergies” delivered from various acquisitions is the fact that interest expense is now about 85% of net income. At some point, the debt here will slow dividends or the company’s ability to continue to grow by acquisition. That’ll be a painful day for shareholders in my view.

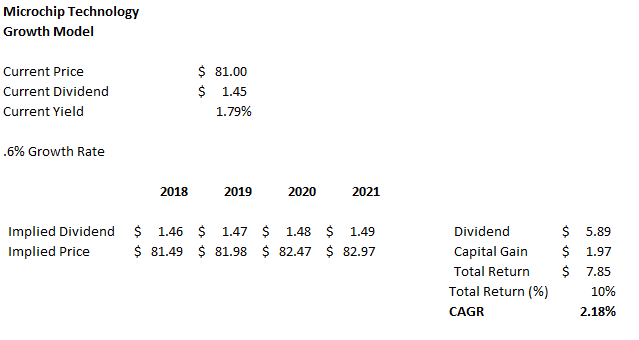

While the financial history offers clues about the most likely financial future (for instance, I spotted the disconnect between revenue and net income earlier and that tradition continues here), investors are most concerned about a future. The past is relevant to some extent, but the fortunes of the marginal buyer (or put buyer) are determined by what happens in the future. It’s with that in mind that I want to make an attempt at modelling a likely future here. Whenever I engage in such a practice, I make a ceteris paribus assumption, holding all constant but the most relevant variable. In my view, the dividend is a good variable to “move”, while holding all else constant, so I’ll infer future stock price by moving it and holding all else (like yield) constant.

Although the amount that the company pays in dividends has grown at a CAGR of about 2.9% over the past six years, the dividends per share have only grown at about .6%, given the high level of dilution here. I’ll continue to assume this growth rate going forward. In my view this is reasonable, given that cash will be needed for growing interest expenses, and (hopefully) some debt reduction.

When I perform this exercise on Microchip, I infer a CAGR growth rate for the shares of only about 2.2% over the next four years. In my view, this is way too little of a return for the various risks present here.

When I perform this exercise on Microchip, I infer a CAGR growth rate for the shares of only about 2.2% over the next four years. In my view, this is way too little of a return for the various risks present here.

Investors seem unaware of history when they place a high value on acquisitions. The optimism they seem to show is strange to me in light of the fact that the vast majority of acquisitions fail (Why do up to 90% of Mergers and Acquisitions Fail?). The fact that acquisitions have a high failure rate is simply a matter of historical fact. A more subtle problem is that they tend to seduce investors into a false sense of optimism because “growth” is the inevitable result of acquisitions. There is certainly growth, but it comes with greater risk (of write down of assets in future, for example).

On the “plus” side of the acquisition scorecard, both earnings and cash flows rise as the acquired company’s cash flows are added to those of the acquirer. On the “minus” side of the scorecard there is the ongoing risk of failure, the risk of goodwill writedowns, the risk that management simply destroyed shareholder value by paying too much for vague ideas like “expanding the Company’s range of solutions, products, and capabilities by extending its served available market.” (Microchip 2017 10-K, pp F-20). Thus, in general, it might be helpful for them if investors read the historical record, and saw that any increased growth comes with increased risk.

In the case of the Atmel acquisition, for example, fully 77% of the acquired assets are intangibles or goodwill. Of the amount paid for intangible assets (as distinct from goodwill), only 34% is customer related intangible assets (contracts, customer loyalty programs and the like). Thus, most of the intangible assets acquired in this transaction relate to technology. This is obviously the source of future revenue, but they are far more risky assets, and thus should be discounted relative to customer intangibles in my view. We investors should apply a steeper discount rate to future cash flows to account for the added risk here.

Technical Snapshot

As per our ChartMasterPro Daily Trade Model, the trend for MCHP turned bearish when it closed below $82.00 on July 21. This signalled a bearish breakdown from an uptrend line on the daily charts which began on July 5. From here we see the shares falling to the $72.00 level over the next three months.

Today we may buy MCHP put options, which will provide us with approximately 16x leverage on our short trade (for details on the option, please visit our website). Our initial stop-loss exit signal will be a daily close above $83.00.

For investors in the shares, we recommend that you sell to avoid any further drop in the share value.

For better or worse, investors rarely access the future cash flows of a given company from the company itself. We access those cash flows via the proxy stock that supposedly represents the fortunes of that business. This negotiation with the “Mr. Market” made famous by Benjamin Graham can be either a blessing or a curse. If the shares are priced pessimistically (i.e. “cheap”), then there might be value there. If, on the other hand, the shares are priced optimistically (i.e. “expensive”), then there’s more downside than upside embedded in the shares. When shares are priced for perfection, great news may not move them very much, as greatness is already “priced in.” if, as is more typical, the company hits a bump in the road, optimistic expectations are dashed and the shares react predictably and inevitably. Thus, it’s a good idea to avoid shares that are optimistically price as they have a badly skewed risk-reward relationship.

The lesson here is that to succeed at stock investing you must be willing to eschew what’s most popular and embrace that which most people would call you crazy for embracing. That’s where future outsize gains come from. It’s not comfortable, but few worthwhile things in life are always comfortable. If you’re buying something because the crowd has bid the shares up, you are buying at the point of maximum danger. That’s a lesson for all investors, including people who are long Microchip Technology Incorporated. These are shares that are best to avoid until the price inevitably drops.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a short position in MCHP over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We trade options. Sometimes our trades last a few days, sometimes a few weeks, sometimes a few months. Please review our trade history listed in our Seeking Alpha BlogPost to get a feel for our trading style.

Top 5 Cybersecurity Influencers to Follow on Twitter in 2017

As we all know, it’s difficult to stay up-to-date with security and threat news. To stay updated with industry news and get in-depth security reports and insights, you need to keep up to date with what the experts are saying.

But who are the experts? Here, I am going to share my list of Top 5 cybersecurity influencers so you can follow them and learn from them on Twitter. For each influencer I selected, I included their Twitter handle, an image and a short synopsis. If you are interested to know more about what makes these guys so influential, you can search for them directly on HYPR.

Twitter Handle: @briankrebs

Brian Krebs is a well-known independent investigative journalist. He is always breaking stories in our industry; providing a calm, rational analysis of every cybersecurity incident he discovers. For more of his insights, we recommend you to read his book titled “Spam Nation”: a New York Times best seller.

Twitter Handle: @Billbrenner70

Bill Brenner is Senior Program Manager for Editorial, Information Security Group at The Akamai Technologies. Bill has contributed to numerous tech websites and publications and served as a member of the Board of Directors for NAISG (National Information Security Group). He engages his Twitter followers with thoughts on world news items and their implications on IT security. Occasionally he also Tweets about his personal blog - the OCD Diaries.

Twitter Handle: @Danielmiessler

Daniel Miessler is an Information Security Practitioner and maintains his website actively which has over 2,500 essays, podcasts, articles, tutorials, posts and more. Every Sunday he shares a curated list of the most interesting stories in InfoSec, technology and humans called “Unsupervised Learnings”. He has over 10K subscribers to his Sunday edition.

Twitter Handle: @e_kaspersky

Eugene is the eponymous founder of one of the world’s biggest cybersecurity companies, Kaspersky Labs. He established Kaspersky Lab in 1997 and has written numerous articles on computer virology and speaks regularly at security seminars and conferences. Far-flung from his humble start as a software engineer, who sold anti-virus solutions to only a handful of buyers, Kaspersky Lab now operates in almost 200 countries; with 30+ regional and country offices worldwide. It is the world’s largest privately held vendor of software security products. He regularly Tweets interesting, educational links from the Kaspersky blog and other popular InfoSec outlets.

Twitter Handle: @Mikko

Mikko Hypponen is the Chief Research Officer (CRO) of F-Secure and a well-known inventor, columnist and TED speaker. He’s been with F-Secure since 1991. He has written his research to the New York Times, Scientific America and Wired and he frequently appears on international TV. He has lectured at Oxford University, Stanford and Cambridge and on top of all of this, he has delivered the most watched computer security talk on the internet.

Hypponen led efforts to defeat notorious security breaches and viruses and is a consultant to several governments on information security. He was selected among the 50 most important people by the PC World Magazine and was included in the FP Global 100 Thinkers list. He is also a member of the board of the Nordic Business Forum and a member of the advisory board of T2.

I thoroughly enjoy reading everything these influencers have to say. I recommend you follow and connect with each influencer, enjoy the banter they provide, the interactions they have and learn about the brands that they advocate.

We hope this list of cybersecurity influencers helps you stay current and if you have any questions, or would like to suggest someone we left off the list, please don’t hesitate to let us know! Also, don’t forget to follow these influential cybersecurity leaders on Twitter. You can find a Twitter List with all 5 here!

Anas Baig is a cybersecurity journalist by profession with a profound interest in online privacy, security and IoT. Follow him on Twitter @anasbaigdm, or email him directly by clicking here.

Note: This blog article was written by a guest contributor for the purpose of offering a wider variety of content for our readers. The opinions expressed in this guest author article are solely those of the contributor and do not necessarily reflect those of GlobalSign

Short Answers to Hard Questions About Clean Coal Technology

Carbon capture and storage has been shown to work in many pilot projects, which generally do not operate at the scale envisioned by proponents as a solution to climate change. So the challenge is scaling it up to larger-capacity power plants. While there are some projects being designed or under construction, at least two power plants currently capture and stores carbon on a commercial scale. One is the SaskPower’s Boundary Dam 3 in Saskatchewan. The other is the Weyburn project, which gets its CO2 from a coal gasification plant in North Dakota and then sends it through a pipeline to the Weyburn oil fields in Saskatchewan for injection. But as The Times’s Ian Austen explained in March, Boundary Dam 3 has run into some problems. After initially saying that the project was working as intended, capturing 90 percent of the plant’s carbon, Cathy Sproule, a member of Saskatchewan’s Legislative Assembly, unveiled confidential documents in November 2015 indicating that the plant was working at only 45 percent of capacity. According to the Times article: “One memo, written a month after the government publicly boasted about the project, cited eight major problem areas. Fixing them, it said, could take a year and a half, and the memo warned that it was not immediately apparent how to resolve some problems.”

Comments

Post a Comment